Key Takeaways

7 Questions to Frame Your LMS Strategy Before selecting or implementing an LMS in finance, these seven questions determine architectural fit

What risks are people-driven vs system-driven?

(Training addresses human behavior control points)

Which roles carry highest regulatory exposure?

(Traders, underwriters, AML investigators require scaled training intensity)

How often do regulations change in your jurisdictions?

(Frequent updates require rapid versioning)

What evidence must survive audits?

(3-year vs 7-year retention requirements)

How centralized should governance be?

(Global consistency vs regional precision)

How much localization is unavoidable?

(Language, jurisdiction, cultural context)

What is the trade-off between automation and human oversight?

(Scale vs accuracy)

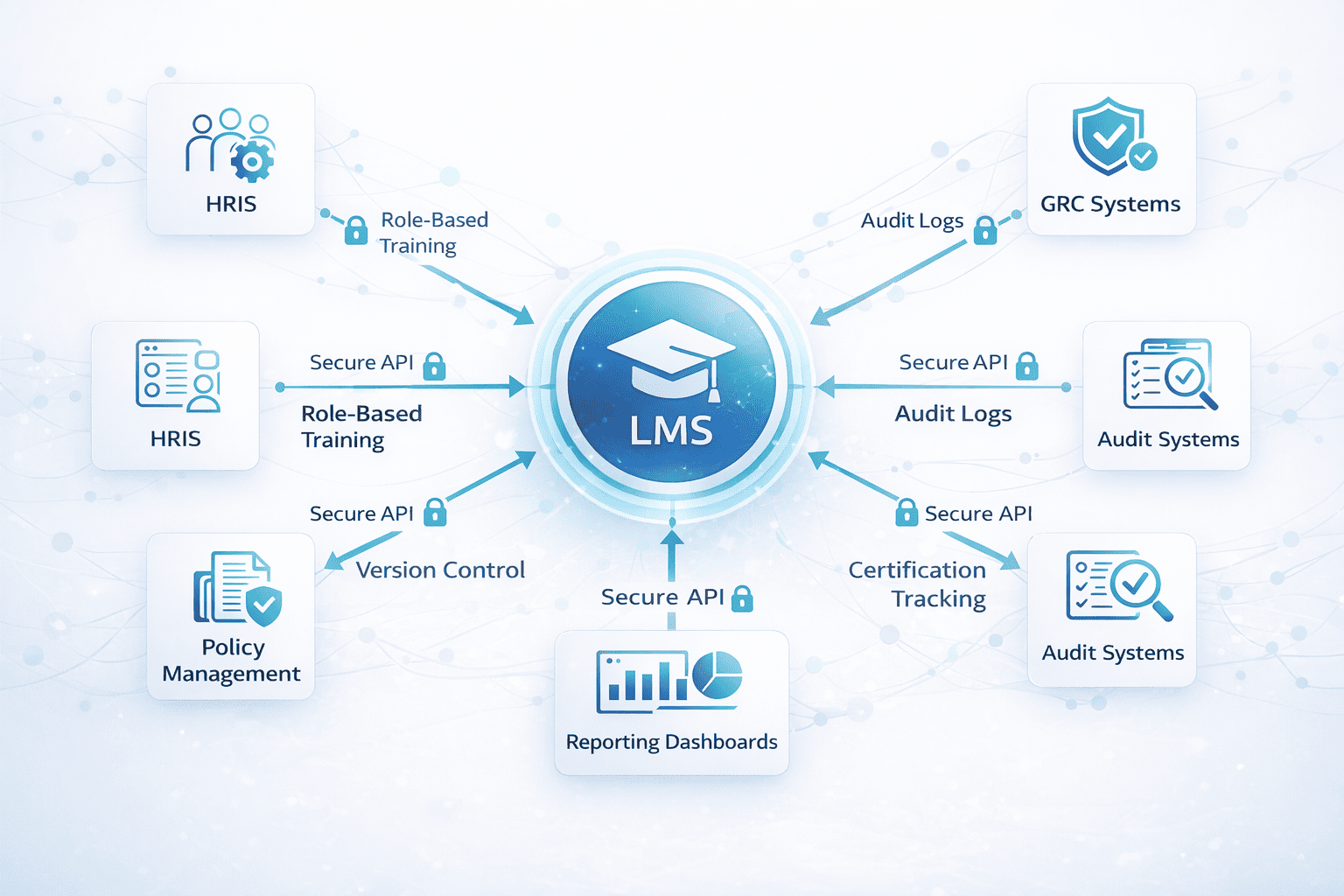

Training isn’t optional in financial services. It’s evidence. Financial institutions operate under continuous regulatory scrutiny where LMS in finance functions as risk control infrastructure, not just training delivery. Banks, insurers, and fintechs must prove employees completed mandatory certifications, certifications remain current, and training content was version-controlled at delivery. The LMS becomes the system of record.

LMS in finance must support audit-grade reporting, time-bound renewals, role-based assignments, and immutable completion logs. The platform sits within a broader GRC ecosystem alongside policy management and risk assessment tools. While Cornerstone and Saba are often the choice for Tier 1 global banks due to deep GRC integrations, audit trail maturity, and enterprise-grade role governance, agile fintechs often lean toward, SimpliTrain, Docebo or Absorb for their superior API flexibility, rapid deployment of sanctions updates, and lighter infrastructure overhead. D2L serves mid-tier regional banks requiring balance between customization and vendor support. The difference: in retail, low completion rates are a training problem. In finance, they’re an audit finding.

Why Do Training and Risk Management Look Different in Financial Institutions?

Financial risk includes human behavior, not just systems. An employee mishandling customer data because they didn’t complete privacy training is a human risk, regulators hold institutions accountable for both. The regulatory expectation is role-specific, consistent training. A trader requires markets conduct training. A mortgage underwriter requires fair lending training. A compliance analyst requires AML training. Each role carries distinct exposure; training obligations reflect that.

The failure modes regulators look for: missed training (assigned but incomplete), expired certifications (not renewed within validity windows), and inconsistent delivery (headquarters updated, branches running outdated content). Each is a control gap. LMS in finance becomes a control mechanism because the platform enforces assignment logic, tracks expirations, and creates audit evidence demonstrating institutional diligence.

Comparison Table: Regulatory Training Models in LMS in Finance

| Model | How It Works | Strengths | Limitations | Typical Use Context |

|---|---|---|---|---|

| Completion-based compliance | Assign course, track completion, log timestamp | Simple audit trail, clear pass/fail | Doesn’t measure understanding, vulnerable to click-through | Annual AML refreshers, general conduct training |

| Role-based risk model | Courses assigned based on job function, location, product line | Targeted relevance, reduced training burden | Requires accurate role data in HRIS, complex mapping logic | Markets conduct for traders, fair lending for loan officers |

| Scenario/simulation-supported | Branching scenarios, decision trees, consequence modeling | Demonstrates applied judgment, harder to game | High authoring cost, longer completion time | Fraud detection, customer complaint handling |

| Microlearning refresh model | 3–5 minute modules, frequent delivery, spaced repetition | Reduces cognitive load, fits workflow interruptions | Can fragment understanding, harder to audit as “complete” training | Sanctions updates, policy changes, regulatory alerts |

Critical Compliance Standards an LMS Must Automate

Regulatory training obligations are role-based, time-bound, and evidence-generating. LMS in finance must automate: Compliance Checklist:

AML/KYC: Annual refreshes with immutable timestamps for transaction monitoring, suspicious activity reporting, and customer due diligence

SOX: Certification windows tied to fiscal reporting cycles for internal controls awareness among financial reporting staff

Sanctions Compliance: High-frequency updates when regimes change, screening procedures and restricted party lists require rapid content deployment

Data Privacy: Version tracking for GDPR/CCPA modules covering consumer data handling, conflicts of interest, and market manipulation

Market Conduct: Role-based logic for traders and underwriters, insider trading, markets conduct, and front-running awareness

The operational distinction: proof of completion vs proof of understanding. Completion evidence (timestamp, user ID, version) satisfies most minimums. Proof of understanding (assessment scores, scenario performance) is required for high-risk roles. LMS in finance must capture both. Certification validity windows create renewal cycles. A trader certified March 1, 2025 with 12-month validity must recertify by February 28, 2026. The LMS flags expiration 60–90 days prior and escalates non-completion.

How Do LMS Platforms Manage Regulatory Training at Scale?

- Role-based learning paths: An employee’s job code, department, and location determine automated course assignments. A California branch manager receives California lending regulations; a New York manager receives New York regulations. Both receive federal AML training.

- Automated assignment and reminders: New hires trigger onboarding paths. Certification expirations trigger renewals 90 days before lapse. Regulatory updates trigger reassignments, when sanctions change, employees handling international transactions receive updated training automatically.

- Time-stamped completions with version control: Every record includes user ID, timestamp, course version, assessment score, IP address. Regulators reviewing three-year-old evidence need to know which version of training was active when the employee completed it.

- Segregation of duties: Administrators assign training but cannot alter completion records. Compliance teams export reports but cannot modify content. Content authors update materials but cannot assign them. This prevents single points of failure.

The most common point of failure in automated assignments isn’t the LMS, it’s data decay in the HRIS. If a trader’s job code isn’t updated during a lateral move from equities to derivatives, they may miss critical market conduct training specific to their new desk, creating a major audit finding.

In a 2023 regulatory review we supported, a Tier 1 bank discovered 18 front-office employees had transferred roles but retained outdated training assignments for 4–6 months because HRIS synchronization was quarterly, not event-driven. The fix: real-time HRIS-to-LMS webhooks triggered by role change events, not batch updates. The lesson: your LMS is only as accurate as your source-of-truth HR data. Most financial services LMS implementations use compliance-centric workflows for regulatory minimums and layer adaptive pathways for development programs above the mandatory baseline.

Centralized vs Localized LMS Governance – How Do Financial Institutions Balance Control

Global institutions face a governance tension: centralized control for consistency vs localized autonomy for regulatory relevance.

- Centralized governance: Corporate compliance controls all content and reporting globally. Single source of truth, efficient at scale. The limitation: local regulatory nuances (German privacy law differs from French) require content variants. Centralized teams bottleneck regional requests.

- Localized governance: Regional teams control content and assignments for their jurisdiction. Training aligns precisely with local regulations, language, and context. The limitation: governance overhead multiplies across 40 country instances. Risk of divergence (one region updates AML, another runs outdated content for months) creates audit exposure.

Most large institutions use hybrid models: centralized governance for global policies, localized execution for jurisdiction-specific regulations. Multi-tenant architectures support this, global administrator controls the platform, regional administrators control regional libraries, reporting rolls up to both.

How Does LMS in Finance Handle Data Security and Privacy?

Training data is employee data and audit evidence. Both require protection.

- Encryption: Training records, scores, and logs are transmitted via TLS and stored encrypted—baseline expectation for any system handling employee PII in regulated environments.

- RBAC: Learners access their own records. Managers access direct reports. Compliance teams access audit reports. Nobody has full visibility—least-privilege principle applied to LMS access itself.

- Data residency: GDPR requires EU employee data remain in EU data centers or transfer under valid mechanisms (SCCs). Similar requirements exist in China, Russia, and other jurisdictions. Secure LMS for banks must offer region-specific hosting or demonstrate compliant flows.

- Separation from transactional data: The LMS doesn’t store customer accounts or proprietary trading information. Training systems and core banking systems operate on different networks, often with different hosting models.

- SaaS vs on-premise: SaaS reduces infrastructure burden but requires vendor due diligence. On-premise gives full control but requires internal patching and certificate rotation. Neither is universally more secure, the question is which risk profile the institution can manage.

What Do Auditors and Regulators Expect from LMS Reporting?

Regulators request evidence exports, they don’t log into your LMS. Evidence requirements:

- Timestamped completion records: user ID, course title, date/time, version, score

- Role mapping: proof assigned training matches job responsibilities

- Content version history: which version was active when Employee X completed it

- Exportable reports: CSV, PDF, Excel, not proprietary formats or screenshots

- Immutable audit logs: system-generated, unalterable records of assignments and completions

LMS in finance becomes an evidence repository. Auditors reviewing a three-year-old complaint verify what training the loan officer completed before the incident.

The operational tension: completion metrics vs competency signals. 100% completion looks good, but if scores average 55% and employees need three attempts, completion masks a competency problem. Sophisticated teams track both, completion for minimums, scores for actual risk.

FAQ

Q1. How is LMS used in finance?

Financial institutions use LMS to manage mandatory regulatory training (AML, KYC, SOX, conduct risk), track certification renewals, generate audit-grade completion evidence, and enforce role-based training requirements. The LMS functions as risk control infrastructure within the GRC ecosystem.

Q2. Can LMS help with AML and KYC training?

Yes. The LMS handles role-based assignment, tracks completion with timestamps and version control, manages certification validity windows, and produces exportable evidence for audits. The platform ensures assignment and documentation, not comprehension.

Q3. Is LMS data secure for financial institutions?

Security depends on implementation. Properly configured platforms use encryption, RBAC, and data residency compliance. SaaS vendors serving financial institutions typically maintain SOC 2 Type II certification. Security requires vendor due diligence and regular reviews.

Q4. What reports do regulators expect from LMS?

Timestamped completion records with user ID, course version, and scores; role-to-training mapping documentation; exportable data in CSV or PDF; immutable audit logs showing assignments and completions. Regulators expect independently verifiable evidence.